Got questions regarding medical bills? You must read this!

Medical bills aren’t uncommon as health issues plague almost everyone. Discover more about the cost of medical procedures, medical debt and the minimum payment on medical bills to understand your financial implications involved. Keep reading!

Did you know that 79 million Americans face problems with medical bills or debt? From minor routine checkups to major life-saving procedures, our healthcare system tackles a variety of health concerns, and we get handed a stack of medical bills to be paid. With 3 out of 4 American workers living paycheck to paycheck, it only takes one medical expense to impact your monthly budget.

Never stress about an unexpected expense again.

same-day loans.

same-day loans.

Health issues can strike at any time even when you do your best to avoid them. Having health insurance helps tremendously but 27 million Americans are uninsured. This opens up even bigger problems with paying medical bills even for the most common medical procedures. In this article we shall get into the nitty gritty of medical bills and minimum payment on medical bills.

What is the minimum monthly payment on medical bills?

When you have medical bills to pay, it is only normal to wonder what your monthly payments would be like just as you’d think about car payments or student loans. So, if you’re wondering what is the minimum monthly payment on medical bills or if there is a medical bills minimum payment law, let’s put your mind at ease.

For starters, there’s no universally accepted amount for minimum payment on medical bills. Your minimum monthly payment on medical bills is dependent on the payment plan a patient and their provider agree upon.

However, that doesn’t mean there aren’t things you can do to improve or help your situation with medical bills.

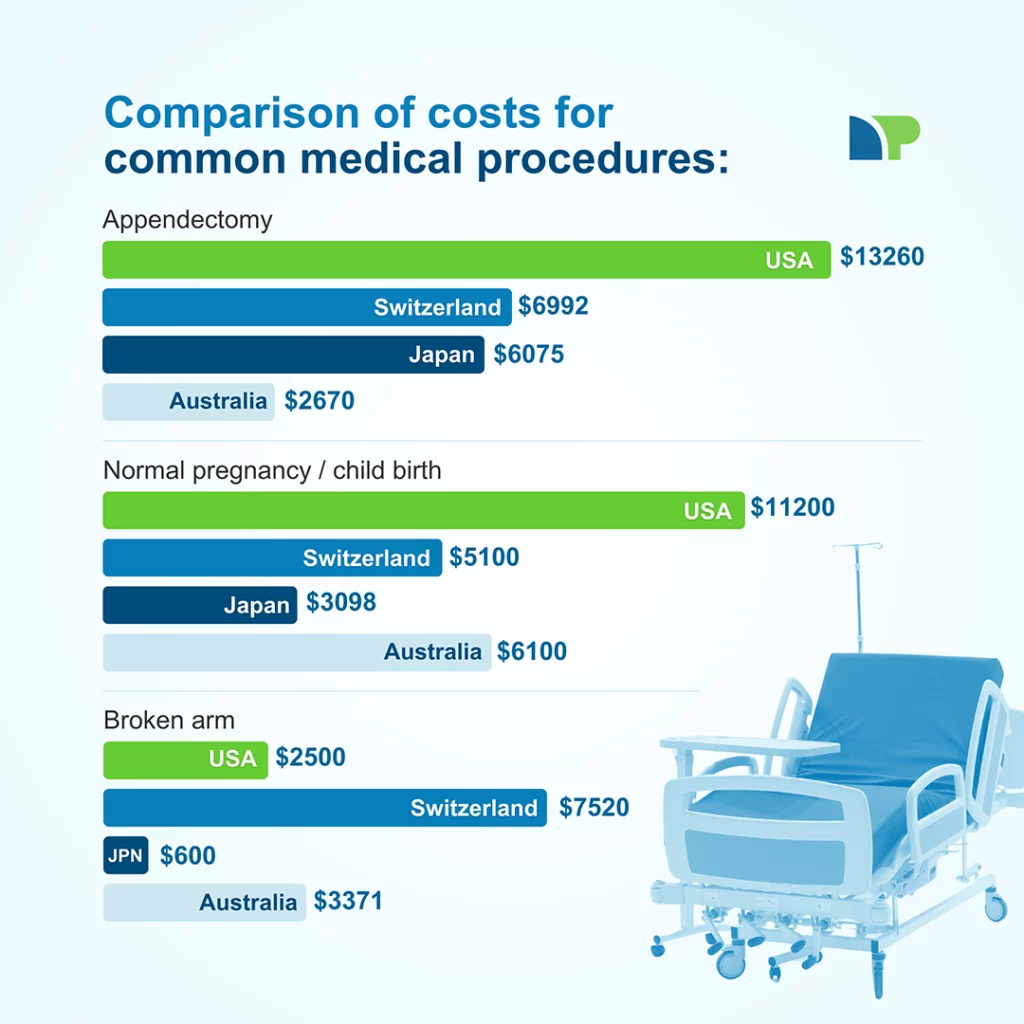

How much do common medical procedures cost?

We did some digging and came up with a cost comparison for common medical procedures in the United States versus and few other countries. Take a look:

The above numbers are obtained from various sources, such as Statistica, compareclub, and others. It’s no secret that medical expenses in the US tend to be expensive! Be aware though that pricing may vary based on several factors such as location, provider, severity of condition, overall health of patient, etc. Please talk to your provider for estimates tailored to your needs for common medical procedures.

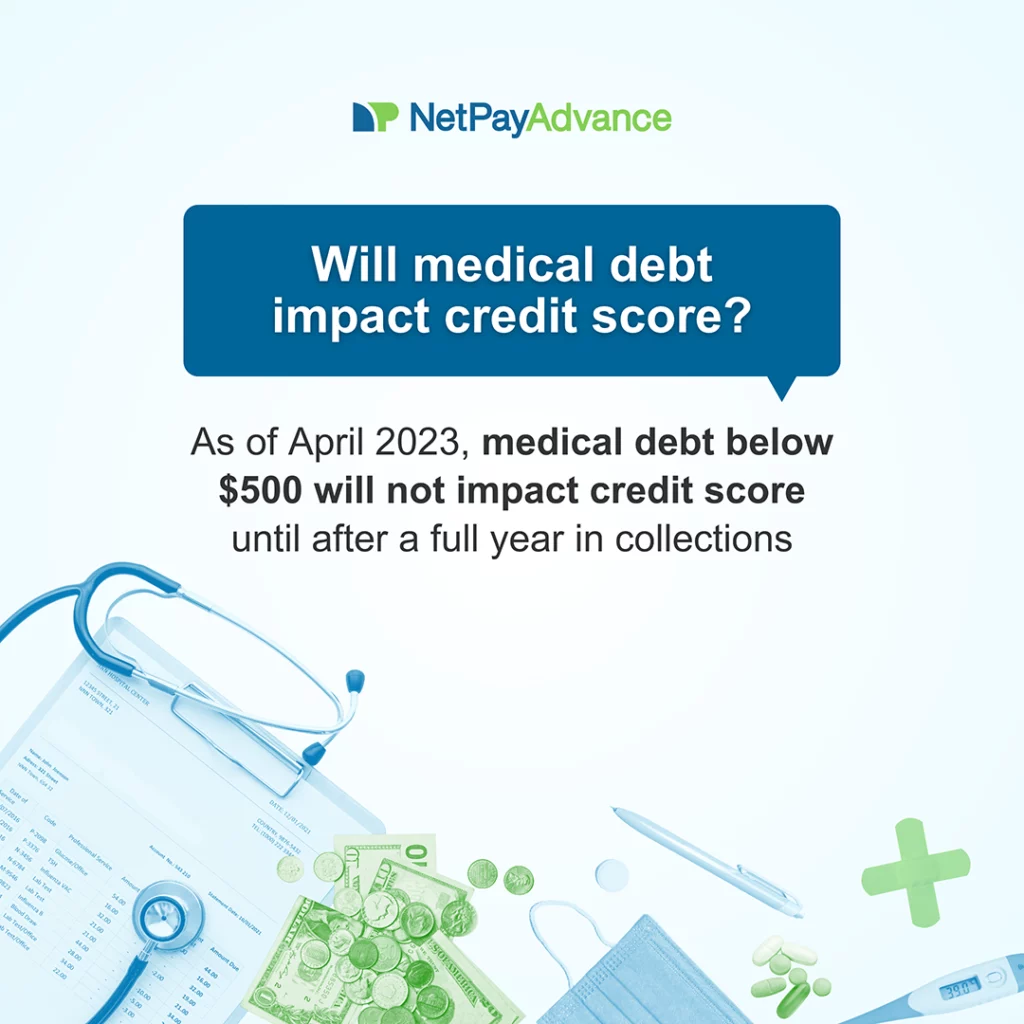

Will medical debt impact credit score?

Medical debt will not impact credit score right away. You have time before your medical debt goes into collections and even after that, you have a solid year.

In April 2023, three consumer reporting companies declared that medical collections below $500 would be removed from credit reports effective on April 11, 2023. It is estimated that around 22.8 million people got at least one medical collection removed from their credit reports while around 15.6 million people got all medical collections removed from their credit reports. Nobody likes dealing with collection agencies. That’s why it is important to do your due diligence before your bills go into collections. There are a few things you can do before your loan goes into collections. These tips will help you secure lower minimum payment on medical bills.

Additional information about your credit

People always want to know when certain bills or debt have an impact on their credit score. It is a valid concern because credit does play a significant role in one’s finances and ability to secure financing. Speaking of credit, did you know you can get a free credit report annually? You can even keep track of your credit by using one of these credit monitoring apps. It is vital to understand your credit score and how credit scores are calculated.

How to get lower rates for minimum payment on medical bills

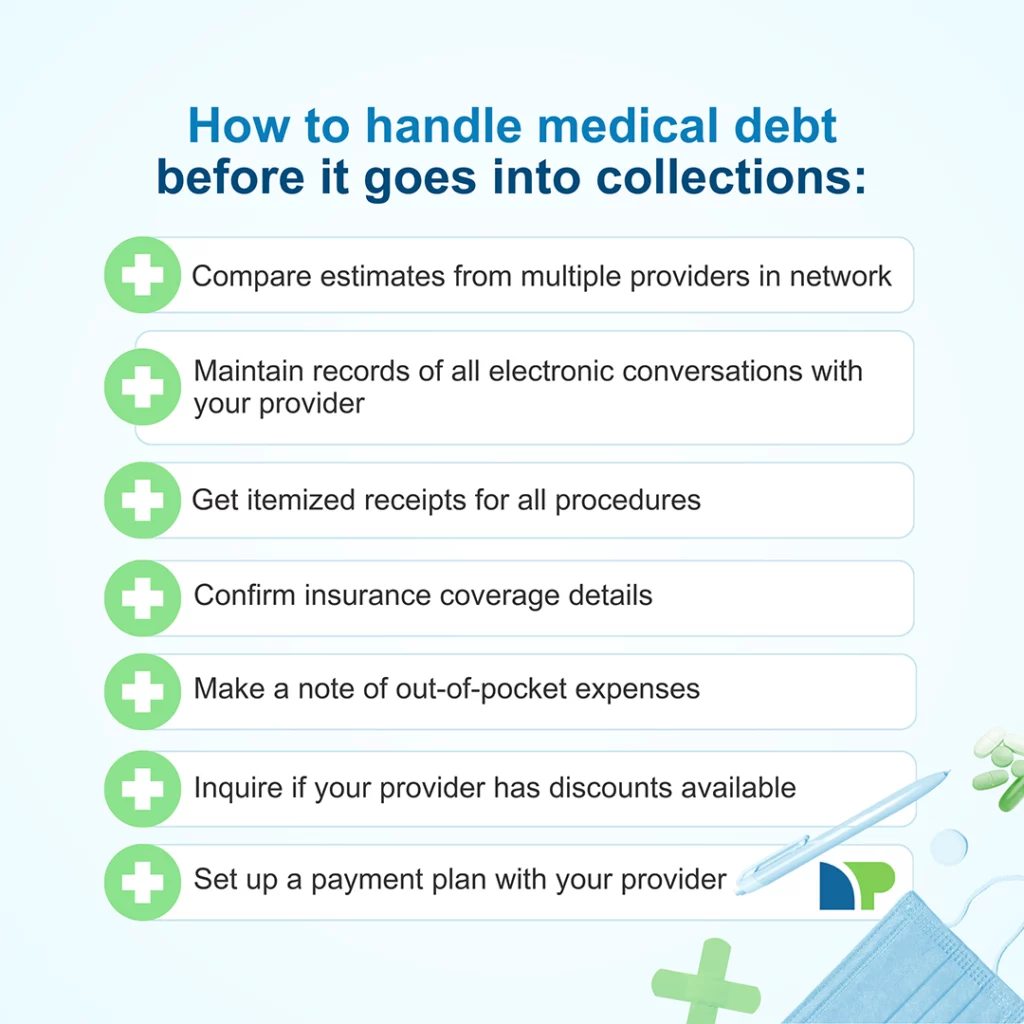

As discussed earlier, there are a few tricks and tips that might help you lower your medical bills and handle medical debt before it goes into collections. Let’s explore them:

It is always a smart idea to do some research when looking to get common medical procedures. It is recommended to get multiple quotes from providers that take your insurance. This allows you to compare estimates and reviews of multiple providers.

Keeping written records of conversations with your provider pertaining to costs will be extremely helpful should you need to dispute a charge.

Asking for an itemized receipt after you receive medical care will show you a complete breakdown of all costs involved. Speak with your insurance company to know how much they’re going to cover so that you have an idea of what you’ll need to pay out of pocket.

Last but not least, always ask your provider for better rates and discounts if available. Work with your provider to pay back the medical debt. Most providers will be happy to set up a payment plan for you where you can pay back the medical debt in installments.

How to deal with medical debt

This is a burning question that plagues millions of Americans across the nation. Even with solid health insurance, people struggle to afford these expenses. I have listed a few ways that help patients, and their families get some relief.

1. Be honest about your situation

Yes, it can feel embarrassing to be vulnerable, but you are not alone. The vast majority of Americans are in the same boat as you. Be upfront about your financial situation if the bill is too large or if you’ve been impacted by a major event such as illness, layoffs, death in the family, etc. Ask about your options. Several hospitals have plans for patients dealing with financial hardships and you might be able to benefit from such a program. If they don’t offer those programs, they may know of some they can recommend that work to provide grants or assistance to low-income consumers. Alternatively, see if you can negotiate for them to remove interest charges.

2. Identify your minimum monthly payment for medical bills

As stated earlier, there’s no universally set monthly minimum for medical debt. Your minimum monthly payment is dependent on factors such as the total debt you owe, your medical provider, and if there is any kind of payment plan. Your minimum monthly payment will depend on the agreement you set up with your medical provider. Review your itemized bill to find the total amount you owe, as well as any potential charges or fees.

3. Negotiate a settlement

Sometimes if you offer to pay a lump sum although lower than what you owe, your provider might take up on that offer. Also, if another provider charges less for the same procedure, you might be able to request a price match from your provider.

If your health provider will allow you to settle your medical debit, be sure to get it in writing. Make sure your settlement agreement clarifies you’ll no longer owe medical debt to that provider if your end of the deal is met.

4. Avoid shocks and surprises

It is an absolute nightmare when a medical bill hits you out of the blue. There is a No Surprises Act in place to protect patients from surprise medical bills. A surprise medical bill can be explained as a bill for out-of-network charges that you didn’t know were out-of-network before getting a service. Such bills can come from hospitals as well as doctors’ offices. Therefore, providers are required to inform patients about the costs involved. Remember, knowledge is power!

5. Watch out for errors

Errors are common in almost all areas of life, and you can never be too careful. Always go through your medical bills and keep an eye out for unauthorized charges or billing errors. Do not be afraid to ask questions. Medical staff are there to help you, including the people in the billing department. Please be sure to review terms and conditions. Your medical bill should clarify your payment terms, penalties if any, additional fees, fines due to failure to pay, and more.

6. Get financial assistance

If you need financial help to afford medical bills, there are several resources available. Check out these options listed on the government website. Depending on your credit score, consider consolidating or refinancing your debt consolidation. Some people with better credit may be able to be approved for a debt consolidation loan, or to do cash-out refinancing on their home.

Sometimes, it might be a while before any of these resources hand you the money to deal with your medical bills. If time is of the essence, you can explore these tried and tested ways to get cash ASAP!

7. Consider a short-term loan

This may not be your first choice but oftentimes, this stands out as the most feasible option. Don’t believe me? Check out what thousands of people are saying about loan products from Net Pay Advance. And the best part is that Net Pay Advance does not do a hard credit check! So, an applicant’s credit score isn’t a considered factor for approval.

See if we offer emergency loans in your state:

See which loan options are available in your state

Bridging the gap

Healthcare is essential to quality of life. It is heartbreaking to see so many people across the country battle health crisis every year. There are excellent medical providers in every state and an army of hardworking professionals trained to offer premier services. We encourage patients to thoroughly research options in their area when it comes to picking a provider for common medical procedures.

Net Pay Advance aims to bridge the gap by providing helpful information and financial help so that you can get the medical treatment you need while armed with knowledge and the empowered with quick funds.

Got questions? Contact us!